Lending Reference Rates

-

Definition

EURIBOR (Euro Interbank Offered Rate) is the rate at which wholesale funds in euro, for periods equal to the relevant interest period of the credit facility, could be obtained by credit institutions in the European Union (EU) and European Free Trade Association (EFTA) countries in the unsecured money market, and published on every TARGET Day[1] by the European Money Markets Institute (EMMI) (or any successor body) at or shortly after 11 a.m. Brussels time. The applicable EURIBOR for a specific interest period is set two Business Days[2]prior to the date of the commencement of such period.

The administrator of EURIBOR is the European Money Markets Institute (EMMI).

Credit facilities dated as of 09/09/2015 or thereafter provide that, in case the relevant EURIBOR is less than zero, then EURIBOR shall be deemed to be zero for the purposes of the credit facility.

Calculation methodology

EURIBOR is calculated following the methodology (referred to as the ‘hybrid methodology’) described in the Benchmark Determination Methodology for EURIBOR (https://www.emmi-benchmarks.eu/benchmarks/euribor/methodology/) and relies on contributions from a panel of credit institutions that are active participants in the euro money markets (Panel Banks) in order to determine the average rate at which wholesale funds in euro could be obtained by credit institutions in the EU and EFTA countries in the unsecured money market.

EURIBOR is grounded, to the extent possible, in euro money market transactions that reflect the Underlying Interest[3]. To ensure robustness in the absence of transactions in the Underlying Interest, the Benchmark Determination Methodology for EURIBOR follows a hierarchical approach consisting of three levels. These levels are employed progressively and in the following order:

- Level 1 consists of contributions based solely on transactions in the Underlying Interest at the Defined Tenor[4] from the prior TARGET Day, using a formulaic approach provided by EMMI.

- Level 2 consists of contributions based on transactions in the Underlying Interest across the money market maturity spectrum and from recent TARGET Days, using a defined range of formulaic calculation techniques provided by EMMI.

- Level 3 consists of contributions based on transactions in the Underlying Interest and/or other data from a range of markets closely related to the unsecured euro money market, using a combination of modelling techniques and/or the Panel Bank’s judgement.

EMMI performs an annual assessment of the EURIBOR methodology. Based on this assessment, EMMI will decide annually on any changes to the EURIBOR methodology. The objective of any change to the methodology is to ensure that the input data and methodology represent the market and economic reality EURIBOR seeks to measure.

Further details on the calculation methodology for EURIBOR, including the factors contributing to a change in the EURIBOR rate can be found in the Blueprint for the Hybrid Methοdology for the Determination of EURIBOR (https://www.emmi-benchmarks.eu/benchmarks/euribor/methodology/) as well as in the abovementioned Benchmark Determination Methodology for EURIBOR.

The Bank has informed its affected clientele with a letter sent in May 2020.You can find the relevant letter here.

For the purposes of this section:

[1] ‘TARGET’ is the Trans‐European Automated Real‐time Gross Settlement Express Transfer System. The Eurosystem maintains TARGET2, which is the second generation of TARGET and is a real‐time gross settlement system. References to “TARGET” should be read with respect to the euro system’s TARGET2 system. ‘TARGET Day’ is a day on which the TARGET system is operating.

[2] ‘Business Day’ is any day (other than a Saturday and Sunday) on which commercial banks in Cyprus are generally open for business and a day on which the TARGET system is operating, unless otherwise defined in the terms of the relevant credit facility.

[3]‘Underlying Interest’: The Underlying Interest for EURIBOR as per EMMI is defined as “the rate at which wholesale funds in euro could be obtained by credit institutions in the EU and EFTA countries in the unsecured money market.”

[4] ‘Defined Tenors’: There are five “Defined Tenors” for EURIBOR, being 1 Week, 1 Month, 3 Months, 6 Months and 12 Months.

-

The ECB Base Rate is the interest rate set by the Governing Council of the European Central Bank (ECB) from time to time during its monetary policy meetings, based on which ECB main refinancing operations of the Eurosystem are carried out through a weekly tender procedure for fixed rate tenders.

The ECB Base Rate may increase or decrease from time to time.

The ECB Base Rate applicable from time to time is published on the website of the ECB https://www.ecb.europa.eu/stats/policy_and_exchange_rates/key_ecb_interest_rates/html/index.en.html

Given that the interest rate of the credit facility includes the ECB Base Rate, the interest rate of the credit facility will change on the effective date of a change in the ECB Base Rate. Any changes to the ECB Base Rate are announced through a press release of the Governing Council of the ECB regarding monetary policy decisions, which is posted on the website of the ECB https://www.ecb.europa.eu/press/pr/activities/mopo/html/index.en.html. Any such change in the ECB Base Rate shall have effect as from the date mentioned in the relevant press release as the date on which the relevant interest rate change shall start and/or from which it shall have effect.

If the ECB Base Rate is less than zero (0) at any time, then the ECB Base Rate applied by the Bank shall be deemed to be zero (0) for the purposes of calculating your interest rate for the period for which the ECB Base Rate is set by the Governing Council of the ECB as being less than zero (0). In such a case, the interest rate that the Bank will apply to the credit facility for that period, shall be ECB Base Rate = zero (0) plus margin.

An update for the change in market interest rate can be found here. The Bank has informed its affected clientele in December 2022.

Bank’s Base Rates – for loans in Euro that have been granted prior to 1 January 2008

The Bank’s Base Rate (BBR) applicable to loans that have been granted prior to the 1st of January 2008 and continue to be in force, is the European Central Bank Base Rate (ECB Base Rate), as defined hereunder:

The ECB Base Rate is the interest rate set by the Governing Council of the European Central Bank (ECB) from time to time during its monetary policy meetings, based on which ECB main refinancing operations of the Eurosystem are carried out through a weekly tender procedure for fixed rate tenders.

The ECB Base Rate may increase or decrease from time to time.

The ECB Base Rate applicable from time to time is published on the website of the ECBGiven that the interest rate of the Loan includes the ECB Base Rate, the interest rate of the Loan will change on the effective date of a change in the ECB Base Rate. Any changes to the ECB Base Rate are announced through a press release of the Governing Council of the ECB regarding monetary policy decisions, which is posted on the website of the ECB https://www.ecb.europa.eu/press/pr/activities/mopo/html/index.en.html. Any such change in the ECB Base Rate shall have effect as from the date mentioned in the relevant press release as the date on which the relevant interest rate change shall start and/or from which it shall have effect. -

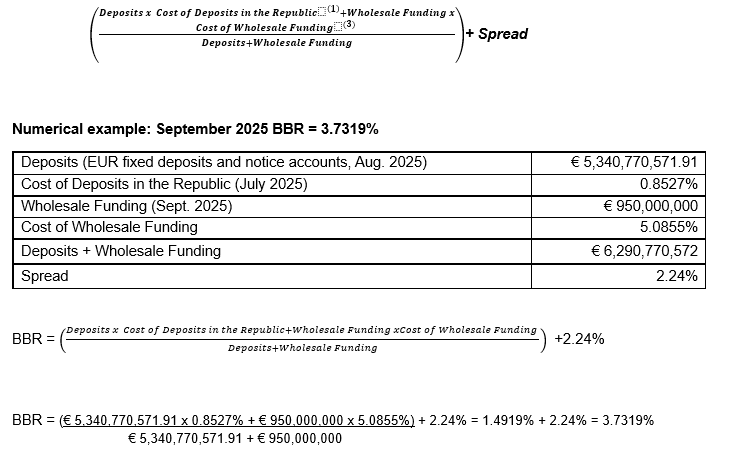

Bank Base Rate (BBR)

The Bank Base Rate (BBR) is calculated as the sum of:

(a) The weighted average of the cost of euro-denominated deposits in the Republic of Cyprus with agreed maturity up to 2 years (according to the Central Bank of Cyprus’ index(1)) and the Bank’s cost of wholesale funding, and

(b) The fixed spread of 2.24%.

The BBR is revised on a quarterly basis (15 March, 15 June, 15 September & 15 December of each year (“Adjustment Dates”)(2).

The Bank Base Rate (BBR) is calculated as follows:

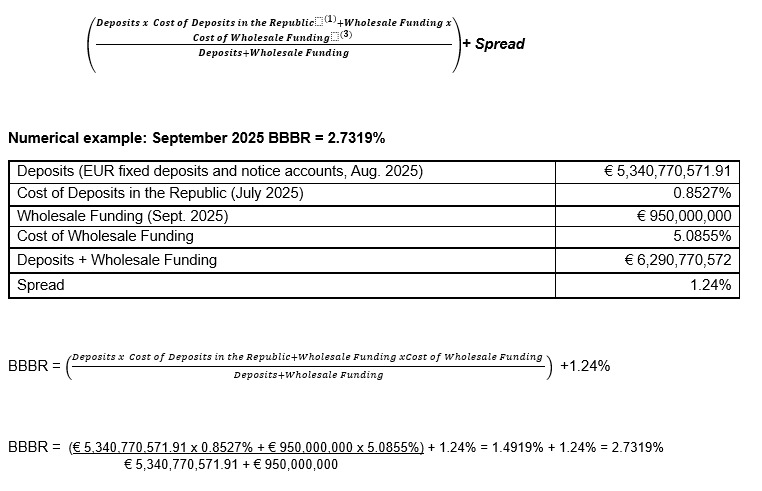

Bank Business Base Rate (BBBR)The Bank Business Base Rate (BBBR) is calculated as the sum of:

(a) The weighted average of the cost of euro-denominated deposits in the Republic of Cyprus with agreed maturity up to 2 years (according to the Central Bank of Cyprus’ index(1)) and the Bank’s cost of wholesale funding, and

(b) The fixed spread of 1.24%.

The BBBR is revised on a quarterly basis (15 March, 15 June, 15 September & 15 December of each year (“Adjustment Dates”)(2).

The Bank of Cyprus’ Base Rate (BBBR) is calculated as follows:

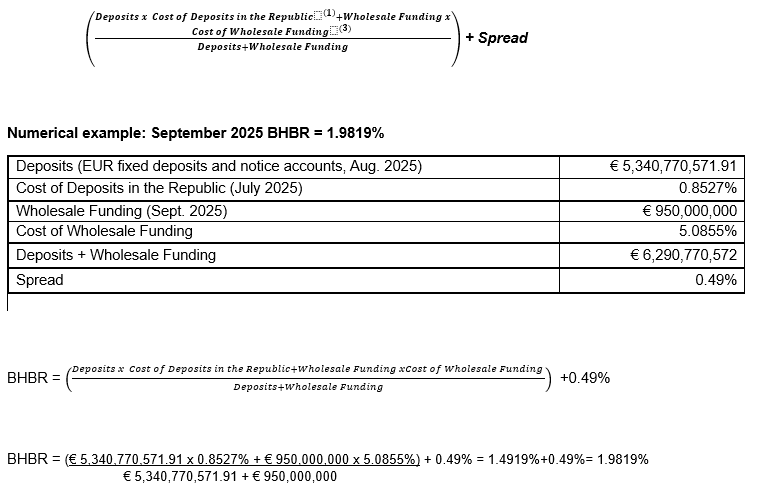

Bank Housing Base Rate (ΒHBR)The Bank Housing Base Rate (BHBR) is calculated as the sum of:

(a) The weighted average of the cost of euro-denominated deposits in the Republic of Cyprus with agreed maturity up to 2 years (according to the Central Bank of Cyprus’ index(1)) and the Bank’s cost of wholesale funding, and

(b) The fixed spread of 0.49%.

The BHBR is revised on a quarterly basis (15 March, 15 June, 15 September & 15 December of each year (“Adjustment Dates”)(2).

The Bank Housing Base Rate (BHBR) is calculated as follows:

Where:

Deposits:

Latest available amount of the Bank’s EUR fixed deposits and notice accounts outstanding as at the review date, as reported to the Central Bank of Cyprus (CBC). This amount can be found on the Bank’s website www.bankofcyprus.com under Bank's Base Rates(3)(Table 1).

Cost of Deposits in the Republic (1) :

Latest release of the interest rate paid on euro-denominated household deposits in the Republic of Cyprus (outstanding amounts) by euro area residents with agreed maturity of up to 2 years, as published on the website of the CBC on a monthly basis. This cost can be found on the Bank’s website www.bankofcyprus.com under Bank's Base Rates (3) (Table 1).

Wholesale Funding:

Total amount of senior unsecured bonds issued by the Bank, outstanding as at the review date of the Bank’s Base Rates. The senior unsecured bonds issued by the Bank from time to time can be found on the Bank’s website at www.bankofcyprus.com under Bank's Base Rates(3) (Table 2).

Cost of Wholesale Funding:

Weighted average cost of Wholesale Funding, outstanding as at the review date of the Bank’s Base Rates. The calculation of this cost can be found on the Bank’s website at www.bankofcyprus.com under Bank's Base Rates(3) (Table 2).

Spread:

- For the Bank Base Rate (BBR), the fixed spread is +2.24%.

- For the Bank Business Base Rate (BBBR), the fixed spread is +1.24%.

- For the Bank Housing Base Rate (BHBR), the fixed spread is +0.49%.

The current Bank Base Rate (BBR), Bank Business Base Rate (BBBR) and Bank Housing Base Rate (ΒHBR), as well as their numerical calculation, as revised on a quarterly basis, are published on the Bank’s website www.bankofcyprus.com in the section Bank's Base Rates(3).

Any change in the methodology of calculating the Bank’s Base Rates may occur if:

- the Central Bank of Cyprus’ index (cost of deposits) ceases to be published, or

- requested by the Regulatory Authority in accordance with the applicable legislation in force from time to time and the monetary and credit rules.

Ιn the case of any change in the methodology of calculating the Bank’s Base Rates, all affected customers / security providers / guarantors will be notified.

The methodology of calculating the Bank’s Base Rates is also published on the Bank’s website www.bankofcyprus.com in the section Bank Base Rates Definition.

The historical evolution and the current Bank’s Base Rates is published on the Bank’s website www.bankofcyprus.com in the section Bank's Base Rates(3).

The latest Bank’s Base rates are displayed here.

(1) Average interest rate paid on euro-denominated deposits from households (outstanding amounts) in the Republic of Cyprus by euro area residents, with agreed maturity of up to 2 years. Published by Central Bank of Cyprus under Monetary and Financial Statistics, Table 10, Deposits from households, with agreed maturity up to 2 years at www.centralbank.cy.

(2) Or the next working day if not a business day.

(3) The historical evolution, the current Bank’s Base Rates, as well as their numerical calculation, as revised on a quarterly basis, are published on the Bank’s website (Home > Personal > Information > Useful links > Other > Bank's Base Rates).

-

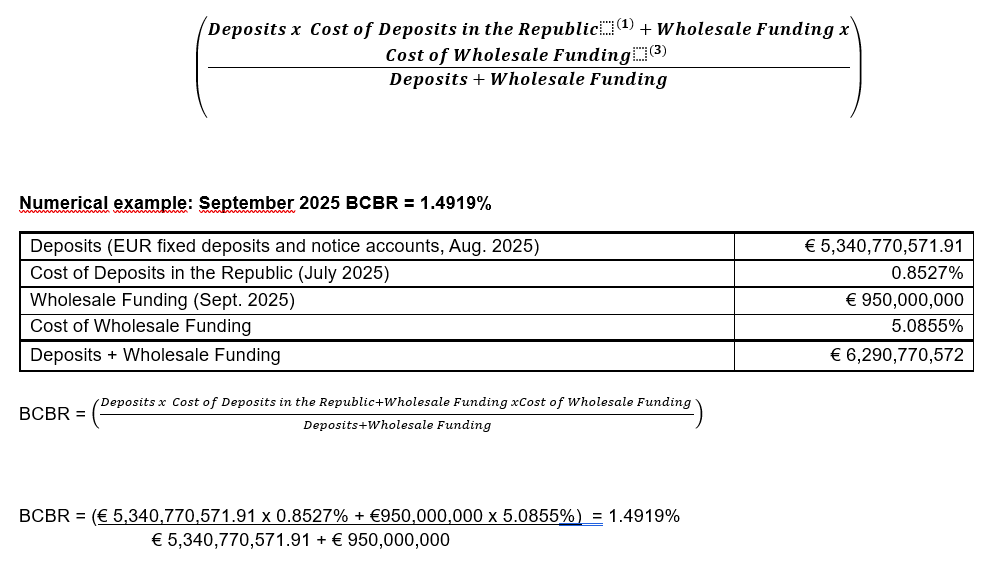

The Bank of Cyprus’ Base Rate (BCBR) is calculated as the weighted average of:

(a) Cost of euro-denominated deposits in the Republic of Cyprus with agreed maturity up to 2 years (according to the Central Bank of Cyprus’ index(1)); and

(b) the Bank’s cost of wholesale funding.

The BCBR is revised on a quarterly basis (15 March, 15 June, 15 September & 15 December of each year (“Adjustment Dates”)(2).

The Bank of Cyprus’ Base Rate (BCBR) is calculated as follows:

Where:

Deposits:

Latest available amount of the Bank’s EUR fixed deposits and notice accounts outstanding as at the review date, as reported to the Central Bank of Cyprus (CBC). This amount can be found on the Bank’s website www.bankofcyprus.com under Bank's Base Rates(3)(Table 1).

Cost of Deposits in the Republic (1) :

Latest release of the interest rate paid on euro-denominated household deposits in the Republic of Cyprus (outstanding amounts) by euro area residents with agreed maturity of up to 2 years, as published on the website of the CBC on a monthly basis. This cost can be found on the Bank’s website www.bankofcyprus.com under Bank's Base Rates (3) (Table 1).

Wholesale Funding:

Total amount of senior unsecured bonds issued by the Bank, outstanding as at the review date of the Bank of Cyprus Base Rate. The senior unsecured bonds issued by the Bank from time to time can be found on the Bank’s website at www.bankofcyprus.com under Bank's Base Rates(3) (Table 2).

Cost of Wholesale Funding:

Weighted average cost of Wholesale Funding, outstanding as at the review date of the Bank of Cyprus Base Rate. The calculation of this cost can be found on the Bank’s website at www.bankofcyprus.com under Bank's Base Rates(3) (Table 2).

The current Bank of Cyprus’ Base Rate (BCBR) as well as its numerical calculation, as revised on a quarterly basis, are published on the Bank’s website www.bankofcyprus.com in the section Bank's Base Rates(3).

Any change in the methodology of calculating the Bank of Cyprus’ Base Rates may occur if:

- the Central Bank of Cyprus’ index (cost of deposits) ceases to be published, or

- requested by the Regulatory Authority in accordance with the applicable legislation in force from time to time and the monetary and credit rules.

Ιn the case of any change in the methodology of calculating the Bank of Cyprus’ Base Rate, all affected customers / security providers / guarantors will be notified.

The methodology of calculating the Bank of Cyprus’ Base Rate is also published on the Bank’s website www.bankofcyprus.com in the section Bank Base Rates Definition.

The historical evolution of the Bank of Cyprus’ Base Rate is published on the Bank’s website www.bankofcyprus.com in the section Bank's Base Rates(3).

The latest Bank’s Base rates are displayed here.

(1) Average interest rate paid on euro-denominated deposits from households (outstanding amounts) in the Republic of Cyprus by euro area residents, with agreed maturity of up to 2 years. Published by Central Bank of Cyprus under Monetary and Financial Statistics, Table 10, Deposits from households, with agreed maturity up to 2 years at www.centralbank.cy.

(2) Or the next working day if not a business day.

(3) The historical evolution, the current Bank of Cyprus Base Rate and its numerical calculation, as revised on a quarterly basis, are published on the Bank’s website (Home > Personal > Information > Useful links > Other > Bank's Base Rates).

-

Term SOFR – for credit facilities in USD

Definition

Term SOFR is a daily set of forward-looking measurements of SOFR (the Secured Overnight Financing Rate) for USD based on market expectations implied from derivatives markets for the relevant tenor (1, 3, 6 or 12 months), administered and published by CME Group Benchmark Administration Limited¹ on each US Government Securities Business Day at approximately 6:00am Eastern time/11:00 am GMT, which is available as of the date which is two Business Days prior to the commencement of the relevant interest period (or where an interest period commences on a day which is not a Cyprus Business Day, the interest rate which would otherwise be applicable if the interest period had commenced on the immediately preceding Cyprus Business Day), for a period equal in length to the interest period or the nearest equivalent period published by the relevant administrator of that rate.

Credit facilities in USD LIBOR dated as of 09/09/2015 or thereafter which have been replaced by Term SOFR, provide that, in case Term SOFR is less than zero, then Term SOFR shall be deemed to be zero for the particular interest period.

Credit facilities in Term SOFR dated as of 21/10/2022 or thereafter, provide that in case Term SOFR is less than zero, then Term SOFR shall be deemed to be zero for the particular interest period.

For the purposes of this section:

‘Business Day’ is a day which is both a Cyprus Business Day and a US Government Securities Business Day.

’Cyprus Business Day’ is a day (other than a Saturday or Sunday) on which commercial banks are open for general business in Cyprus.

‘SOFR’ is the Secured Overnight Financing Rate administered and published by the Federal Reserve Bank of New York at approximately 8:00 am (ET) Eastern time on each US Government Securities Business Day which reflects a broad measure of the cost of borrowing cash overnight collateralized by Treasury securities.

‘US Government Securities Business Day’ is any day except for (i) a Saturday, (ii) a Sunday or (iii) a day on which the Securities Industry and Financial Markets Association, or any successor thereto, recommends that the fixed income departments of its members be closed for the entire day for purposes of trading in US government securities.

¹Disclaimer:

CME GROUP market data is used under license as a source of information for certain BANK OF CYPRUS PUBLIC COMPANY LIMITED products. CME GROUP has no other connection to BANK OF CYPRUS PUBLIC COMPANY LIMITED products and services and does not sponsor, endorse, recommend or promote any BANK OF CYPRUS PUBLIC COMPANY LIMITED products or services. CME GROUP has no obligation or liability in connection with the BANK OF CYPRUS PUBLIC COMPANY LIMITED products and services. CME GROUP does not guarantee the accuracy and/or the completeness of any market data licenced to BANK OF CYPRUS PUBLIC COMPANY LIMITED and shall not have any liability for any errors, omissions, or interruptions therein. There are no third-party beneficiaries of any agreements or arrangements between CME GROUP and BANK OF CYPRUS PUBLIC COMPANY LIMITED.

Calculation methodology

The calculation methodology for CME Term SOFR can be found in the below link https://www.cmegroup.com/market-data/files/cme-term-sofr-reference-rates-benchmark-methodology.pdf

Daily Non Cumulative Compounded RFR (or as otherwise called Compounded RFR) - for credit facilities in USD

Definition

Daily Non Cumulative Compounded RFR (or as otherwise called Compounded RFR) is, for any RFR Business Day during an interest period, the percentage rate per annum determined by the Bank in accordance with the methodology set out here.

Credit facilities in USD LIBOR dated as of 09/09/2015 or thereafter which have been replaced by the Compounded RFR, provide that, if on any day during an interest period the underlying RFR used to calculate Compounded RFR is less than zero, then the underlying RFR shall be deemed to be zero for that date.

Credit facilities in Compounded RFR dated as of 21/10/2022 or thereafter, provide that if on any day during an interest period the underlying RFR used to calculate Compounded RFR is less than zero, then the underlying RFR used to calculate Compounded RFR shall be deemed to be zero for that day.

For the purposes of this section:

‘RFR’ is a risk free rate which for USD is the SOFR (Secured Overnight Financing Rate) reference rate administered and published by the Federal Reserve Bank of New York at approximately 8:00am (ET) Eastern time on each RFR Business Day which reflects a broad measure of the cost of borrowing cash overnight collateralized by Treasury securities.

‘RFR Business Day’ is any day except for (i) a Saturday, (ii) a Sunday or (iii) a day on which the Securities Industry and Financial Markets Association, or any successor thereto, recommends that the fixed income departments of its members be closed for the entire day for purposes of trading in US government securities.

Calculation methodology

The calculation methodology can be found in the below link

-

Term SONIA - Term Rate for credit facilities in GBP

Definition

Term SONIA is the risk-free interest rate for Sterling over the relevant forward-looking tenor (as implied by overnight index swap contracts that reference SONIA) administered and published by Refinitiv Benchmark Services (UK) Limited on each London business day at 11:50am London time, which is available as of the date which is two Business Days prior to the commencement of the relevant interest period (or where an interest period commences on a day which is not a Cyprus Business Day, the interest rate which would otherwise be applicable if the interest period had commenced on the immediately preceding Cyprus Business Day), for a period equal in length to the interest period or the nearest equivalent period published by the relevant administrator of that rate.

Credit facilities in GBP LIBOR dated as of 09/09/2015 or thereafter

- which have been replaced by Term SONIA, provide that, in case Term SONIA is less than zero, then Term SONIA shall be deemed to be zero for the particular interest period.

- which have been replaced by Term SONIA plus CAS, provide that, in case Term SONIA plus CAS is less than zero, then Term SONIA plus CAS shall be deemed to be zero for the particular interest period.

Credit facilities in Term SONIA dated as of 1/1/2022 or thereafter, provide that in case Term SONIA is less than zero, then Term SONIA shall be deemed to be zero for the particular interest period.

For the purposes of this section:

’Business Day’ is a day (other than a Saturday or Sunday) on which commercial banks are open for general business in Cyprus and London.

’CAS’ is the credit adjustment spread value which is, in respect of the relevant interest period tenor, the percentage rate per annum (as defined by ISDA based on a historical median over a five-year lookback period calculating the difference between LIBOR and SONIA), fixed and published by Bloomberg Index Services Limited on 5 March 2021.

’Cyprus Business Day’ is a day (other than a Saturday or Sunday) on which commercial banks are open for general business in Cyprus.

’SONIA’ is the Sterling Overnight Index Average reference rate administered and published by the Bank of England at 9:00 am London time on each London business day and which reflects the average of the interest rates that banks pay to borrow sterling overnight from other financial institutions and institutional investors.

Calculation methodology

The calculation methodology for Refinitiv Term SONIA can be found in the below link https://www.refinitiv.com/content/dam/marketing/en_us/documents/methodology/term-sonia-methodology.pdf

Daily Non Cumulative Compounded RFR (or as otherwise called Compounded RFR) - for credit facilities in GBP

Definition

Daily Non Cumulative Compounded RFR (or as otherwise called Compounded RFR) is, for any RFR Business Day during an interest period, the percentage rate per annum determined by the Bank in accordance with the methodology set out here.

Credit facilities in GBP LIBOR dated as of 09/09/2015 or thereafter which have been replaced by the Compounded RFR plus CAS, provide that, if on any day during an interest period the aggregate of the RFR underlying the calculation of the Compounded RFR and the applicable CAS is less than zero, then the underlying RFR shall be deemed to be such a rate that the aggregate of the underlying RFR and the applicable CAS is zero.

Credit facilities in Compounded RFR dated as of 1/1/2022 or thereafter, provide that if on any day during an interest period the underlying RFR used to calculate Compounded RFR is less than zero, then the underlying RFR used to calculate Compounded RFR shall be deemed to be zero for that day.

For the purposes of this section:

’CAS’ is the credit adjustment spread value which is, in respect of the relevant interest period tenor, the percentage rate per annum (as defined by ISDA based on a historical median over a five-year lookback period calculating the difference between LIBOR and SONIA), fixed and published by Bloomberg Index Services Limited on 5 March 2021.

‘RFR’ is a risk free rate which for GBP is the SONIA (Sterling Overnight Index Average) reference rate administered and published by the Bank of England at 9:00 am London time on each RFR Business Day and which reflects the average of the interest rates that banks pay to borrow sterling overnight from other financial institutions and institutional investors.

‘RFR Business Day’ is a day (other than a Saturday or Sunday) on which commercial banks are open for general business in London.

Calculation methodology

The calculation methodology can be found in the below link

-

Definition

TORF is an interest rate benchmark based on the data of derivative transactions whose underlying asset is the ‘uncollateralized overnight call rate’ which contains almost no credit risk of financial institutions.

TORF is published for tenors of 1 month, 3 months, 6 months around 17:00 JST (Japan Standard Time) on a Tokyo business day (being term TONA or such other forward looking term rate as is notified by the Bank to the Customer in writing as the most suitable interest rate to apply to the facility), which is available as of the date which is two Business Days prior to the commencement of the relevant interest period (or where an interest period commences on a day which is not a Cyprus Business Day, the interest rate which would otherwise be applicable if the interest period had commenced on the immediately preceding Cyprus Business Day) for a period equal in length to the interest period or the nearest equivalent period published by the relevant administrator of that rate.

The administrator of TORF is QUICK Benchmarks Inc (QBS).

Credit facilities in JPY LIBOR dated as of 09/09/2015 or thereafter

- which have been replaced by TORF, provide that, in case TORF is less than zero, then TORF shall be deemed to be zero for the particular interest period.

- which have been replaced by TORF plus CAS, provide that, in case TORF plus CAS is less than zero, then TORF plus CAS shall be deemed to be zero for the particular interest period.

For the purposes of this section:

‘Business Day’ is a day (other than a Saturday or Sunday) on which commercial banks are open for general business in Cyprus and Tokyo.

’CAS’ is the credit adjustment spread value which is, in respect of the relevant interest period tenor, the percentage rate per annum (as defined by ISDA based on a historical median over a five-year lookback period calculating the difference between LIBOR and TONA), fixed and published by Bloomberg Index Services Limited on 5 March 2021.

’Cyprus Business Day’ is a day (other than a Saturday or Sunday) on which commercial banks are open for general business in Cyprus.

‘TONA’ is the Tokyo Overnight Average Rate administered and published around 10am JST each Tokyo business day by the Bank of Japan and which reflects the uncollateralized overnight call rate.

Calculation methodology

The calculation methodology for TORF can be found in the below link

https://www.torf.co.jp/wp-content/uploads/TORFMethodologyEN.pdf

-

SARON Compound Rate - Last Reset RFR Rate for credit facilities in CHF

Definition

SARON Compound Rate is the compounded average of the daily SARON for a period equal in length to the preceding interest period or the nearest equivalent period, administered and published by SIX Swiss Exchange (and only to the extent that the rate is published and available for that period), two Business Days prior to the commencement of the relevant interest period (or where an interest period commences on a day which is not a Cyprus Business Day, the interest rate which would otherwise be applicable if the interest period had commenced on the immediately preceding Cyprus Business Day).

Credit facilities in CHF LIBOR dated as of 09/09/2015 or thereafter

- which have been replaced by SARON Compound Rate, provide that, in case SARON Compound Rate is less than zero, then SARON Compound Rate shall be deemed to be zero for the particular interest period.

- which have been replaced by SARON Compound Rate plus CAS, provide that, in case SARON Compound Rate plus CAS is less than zero, then SARON Compound Rate plus CAS shall be deemed to be zero for the particular interest period.

For those Clients not signing the Addendum Agreement, please see below the EU Regulation on the designation of a statutory replacement rate for certain settings of CHF LIBOR: https://eur-lex.europa.eu/legal-content/EN/TXT/PDF/?uri=CELEX:32021R1847&from=EN

For the purposes of this section:

‘Business Day’ is a day (other than a Saturday or Sunday) on which commercial banks are open for general business in Cyprus and Zurich.

’CAS’ is the credit adjustment spread value which is, in respect of the relevant interest period tenor, the percentage rate per annum (as defined by ISDA based on a historical median over a five-year lookback period calculating the difference between LIBOR and SARON), fixed and published by Bloomberg Index Services Limited on 5 March 2021.

’Cyprus Business Day’ is a day (other than a Saturday or Sunday) on which commercial banks are open for general business in Cyprus.

‘SARON’ is the Swiss Average Rate Overnight administered and published by SIX Swiss Exchange for the first time at 08.30am Zurich time and for the last time at the end of the trading day. Specifically, SARON is continually calculated in real time and published every 10 minutes and a fixing is conducted three times a day at 12 pm, 4 pm and 6 pm Zurich time on each Zurich business day, which reflects concluded transactions and binding quotes of the underlying Swiss repo market.

Calculation methodology

The calculation methodology for SARON Compound Rate can be found in the below link

Daily Non Cumulative Compounded RFR - for credit facilities in CHF

Definition

Daily Non Cumulative Compounded RFR is, for any Business Day during an interest period, the percentage rate per annum determined by the Bank in accordance with the methodology set out here.

Credit facilities in CHF LIBOR dated as of 09/09/2015 or thereafter which have been replaced by the Daily Non Cumulative Compounded RFR plus CAS, provide that, if the aggregate of the RFR underlying the calculation of the Daily Non Cumulative Compounded RFR and the applicable CAS is less than zero, then the underlying RFR shall be deemed to be such a rate that the aggregate of the underlying RFR and the applicable CAS is zero.

For those Clients not signing the Addendum Agreement, please see below the EU Regulation on the designation of a statutory replacement rate for certain settings of CHF LIBOR:

https://eur-lex.europa.eu/legal-content/EN/TXT/PDF/?uri=CELEX:32021R1847&from=EN

For the purposes of this section:

‘Business Day’ is a day (other than a Saturday or Sunday) on which commercial banks are open for general business in Zurich.

’CAS’ is the credit adjustment spread value which is, in respect of the relevant interest period tenor, the percentage rate per annum (as defined by ISDA based on a historical median over a five-year lookback period calculating the difference between LIBOR and SARON), fixed and published by Bloomberg Index Services Limited on 5 March 2021.

‘RFR’ is a risk free rate which for CHF is the SARON (Swiss Average Rate Overnight) reference rate administered and published by SIX Swiss Exchange for the first time at 8.30am Zurich time and for the last time at the end of the trading day. Specifically, SARON is continually calculated in real time and published every 10 minutes and a fixing is conducted three times a day at 12 pm, 4 pm and 6 pm Zurich time on each Business Day, which reflects concluded transactions and binding quotes of the underlying Swiss repo market.

Calculation methodology

The calculation methodology can be found in the below link

Further information on the above reference interest rates can be found on the following websites:

CBC benchmark rate: www.centralbank.cy

Euribor: www.emmi-benchmarks.eu

SARON, SARON Compound Rate: https://www.six-group.com

SOFR: https://www.newyorkfed.org/markets/reference-rates/sofr

SONIA: https://www.bankofengland.co.uk

Term SOFR: https://www.cmegroup.com/market-data/cme-group-benchmark-administration/term-sofr.html

Term SONIA: https://www.refinitiv.com

TONA: https://www.boj.or.jp

TORF: https://www.torf.co.jp